Running and operating a company is a vital responsibility as there are plenty of compliances and regulations along with tax laws that your business will have to abide by. The role of the auditor of the company is to maintain such abstract compliances. They should also ensure that the company is registered or not.

Company registration in India must be initiated with required documents as per the companies act, 2013. Auditor’s role in the company is crucial as it helps make sure the business’s productivity and efficiency. Also, the companies act, 2013 offers auditors with specific roles, responsibilities, and rights. Hence, what role does an auditor play in the company? Now, you will get the answer to this question in this blog.

Defining auditor as per the company law.

The auditor is a trained person who checks, reviews, and verifies the accuracy and veracity of financial records that the companies have kept. These persons also assist companies in ensuring they comply with Indian tax laws and safeguard businesses from fraud. They also highlight the discrepancies in the business’s financial documents and accounting methods and assist them in maintaining wholesome compliance. If an auditor is an employee of any organization, then he/she can be known as an internal auditor. The role of the internal auditor of the company is to assist the business in staying compliant and in managing their taxes efficiently.

According to section 139(1) of the companies act, all companies are obliged to appoint either individuals or firms to act as their auditors. This signifies the significance of the auditor in the company. The said act also offers auditors with several statutory powers by which they can perform their responsibility and roles efficiently. According to the service agreement, auditors of partnership firms, sole proprietorships, and other organizations will have powers and duties.

What are some of the roles and duties of an auditor in the company?

The auditor’s role is to help a business maintain its financial statements by verifying and reviewing its financial documents. Thus, an auditor’s opinion can be a game-changing factor for the business and its trustworthiness and credibility related to the business’s financial information. In comparison to unaudited statements, audited ones hold a high degree of trust and credibility. Now, let’s look into the auditors’ duties as stated in section 143 of the companies act, 2013.

– Making the audit report.

All auditors are assigned to make an audit report that serves as an appraisal of the company’s current financial position using its financial statements. The accounting books which the auditor has audited have to be maintained according to relevant accounting standards. Also, the auditor should make sure the statements reflect an accurate representation of the company’s financial position.

– Makes critical remarks whenever required.

As the auditor’s report is taken as a reliable source, the auditor should offer an accurate opinion at all times. If they feel that statements do not represent the accurate picture, then they should form a dissenting opinion and state it in the report. And he/she feels dissatisfied with the information given, and then they might issue a disclaimer and restraint from expressing any of their opinions.

– Make inquiries.

An auditor’s role in the company needs them to make inquiries and, as and when required, related to advances, loans, personal expenses charged to the revenue account and deposits made.

– Providing helping hands in branch audit.

If they are the branch auditors and not the company auditors, they should assist other branches in their audits. The auditor should prepare the audit report relying on the branch’s financial statements and send them to the company’s auditor. The company auditor then uses and incorporates this into the fundamental audit report.

– Compliance with auditing standards.

All the auditors should comply with the auditing standards that have been issued by the central government and national financial reporting authority. Such standards assist auditors in executing their duties with accuracy and attain higher efficiency in their work.

– Reporting fraud.

If the auditor gets to know that fraud is taking place within the company, they should report them to the central government. It could happen in situations wherein the figures in the company’s financial statements do not add up. The auditor should report the fraud to an audit committee according to section 177 by stating the fraud’s nature, approximate involved amount and details, names of the parties involved. This applies to cost auditors and secretarial auditors under section 148 and section 204 of the companies act, 2013.

– Compliance with code of professional conduct and ethics.

The appointment of auditor under Companies Act requires one to comply with codes related to professional and ethical conduct. This includes maintaining confidentiality, being vigilant against frauds and errors, and executing duties diligently—also, professional scepticism for better efficiency and accuracy in the work.

– Helping in the investigations.

If the company is under the radar of the investigation, the auditor must provide help to the investigating officers.

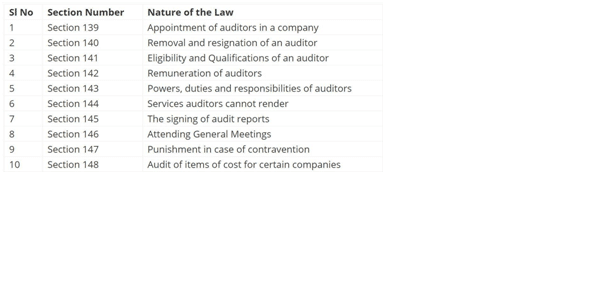

Auditors’ roles according to companies act, 2013 in India.